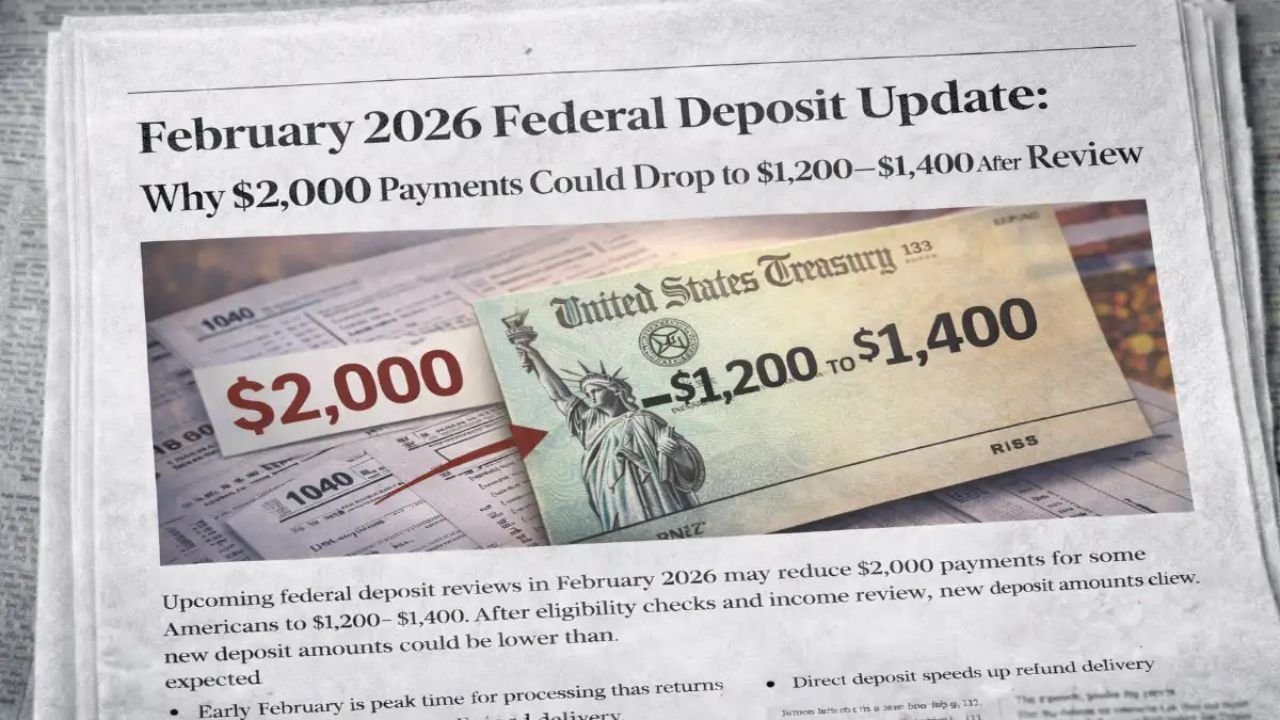

As February 2026 approaches, renewed attention is turning toward federal deposits that many households expect to see reflected in their bank accounts. Online discussions frequently reference a $2,000 payment figure, but official reviews and eligibility checks mean that not every recipient will ultimately receive that amount. For a portion of beneficiaries, final deposits may adjust downward, commonly landing in the $1,200 to $1,400 range once reviews are complete.

Understanding why these adjustments happen and who may be affected is essential for realistic financial planning. Federal deposits are not flat, universal payouts. They are calculated outcomes based on eligibility rules, income data, and compliance checks that aim to balance fairness with fiscal responsibility.

Why Federal Deposits Are Reviewed Before Release

Federal payment programs operate under strict regulatory frameworks. Before funds are issued, agencies conduct routine reviews to confirm that recipients still meet the qualifying conditions. These checks are not new, but in 2026 they are more data-driven than in previous years.

The review process typically evaluates updated income records, recent tax filings, benefit histories, and household changes. Advances in data matching now allow agencies to compare information across multiple systems, reducing the risk of overpayments while increasing accuracy.

For recipients, this means that an initially projected amount may change once the review confirms final eligibility. The goal is not to reduce payments arbitrarily, but to ensure that public funds align with current financial realities.

How the $2,000 Figure Became So Common

The $2,000 amount has strong psychological resonance. During the pandemic era, round-number stimulus payments became familiar, and that association continues to influence public expectations. In reality, many February deposits approach that level because they combine multiple components, such as tax refunds, credits, or monthly benefits.

When preliminary estimates circulate online, they are often interpreted as guaranteed payouts rather than maximum or illustrative figures. Once official reviews apply income thresholds and eligibility formulas, the final amount may differ, sometimes significantly.

Why Payments May Adjust to $1,200–$1,400

Several factors can lead to a reduced deposit after review. Income is one of the most influential. Recipients whose earnings have increased since their last assessment may no longer qualify for the highest payment tier. Even moderate income growth can shift a household into a lower benefit range.

Prior overpayments also play a role. If a recipient previously received an advance payment or excess benefit, the system may automatically offset that amount against the new deposit. These adjustments often surprise recipients, even though they are part of standard program rules.

Changes in household size, filing status, or dependency claims can further affect calculations. When these variables are updated, the system recalculates eligibility using the most recent data available, sometimes resulting in a lower final payment.

Who Is Most Likely to See Adjustments

Not all recipients face the same likelihood of changes. Adjustments are more common among households that have experienced recent income increases, especially those moving from part-time to full-time work or adding a second income earner.

Individuals who updated tax information late, corrected prior filings, or reconciled advance credits may also see revised amounts. In contrast, lower-income households with stable financial profiles are more likely to receive amounts close to initial expectations.

It is important to note that a reduced payment does not indicate an error or penalty. In most cases, it reflects updated eligibility data being applied as intended.

February 2026 Payment Timing and Release Windows

Federal deposits in February are typically released in stages rather than on a single date. Direct deposit recipients generally receive funds first, followed by those using prepaid cards or alternative electronic methods. While some programs still offer mailed payments, electronic delivery remains the fastest and most reliable option.

The shorter calendar month can slightly shift payment timing, occasionally making deposits appear earlier or later than anticipated. Review-related adjustments may also delay certain payments by a few days while final calculations are completed.

How to Reduce the Risk of Delays or Errors

While recipients cannot control eligibility formulas, they can take steps to minimize processing issues. Ensuring that banking information is current is critical, as outdated account details remain one of the most common causes of delays.

Filing required tax returns on time and reviewing benefit notices carefully can also prevent complications. When agencies request verification or additional documentation, responding promptly helps keep payments on schedule.

Financial advisors recommend avoiding firm plans around a specific deposit amount or date. Treating federal payments as supplemental rather than guaranteed income provides greater flexibility if adjustments occur.

Separating Expectations From Reality

Disappointment often stems from expectations shaped by headlines rather than official rules. Federal deposits are calculated outcomes, not promises of uniform amounts. Understanding this distinction can reduce stress and help households plan more effectively.

The shift toward more rigorous reviews reflects broader policy goals of accuracy and sustainability. While adjustments may feel inconvenient in the short term, they are designed to reduce errors, fraud, and future repayment issues.

Final Outlook for February 2026 Deposits

February 2026 does not introduce a new universal $2,000 payment program. Instead, it highlights how existing federal systems apply eligibility reviews to determine final deposit amounts. For some recipients, that will mean receiving the full projected amount. For others, adjustments may bring payments closer to $1,200 or $1,400 based on updated information.

Staying informed, maintaining accurate records, and approaching federal deposits with realistic expectations remain the best strategies. In an environment shaped by data-driven reviews, clarity and preparation are the most reliable safeguards.

Disclaimer

This article is for informational purposes only and does not constitute financial, legal, or tax advice. Federal payment amounts, eligibility requirements, and timelines are governed by official laws and agency regulations and may vary based on individual circumstances. Readers should consult official government sources or qualified professionals for the most accurate and personalized guidance.